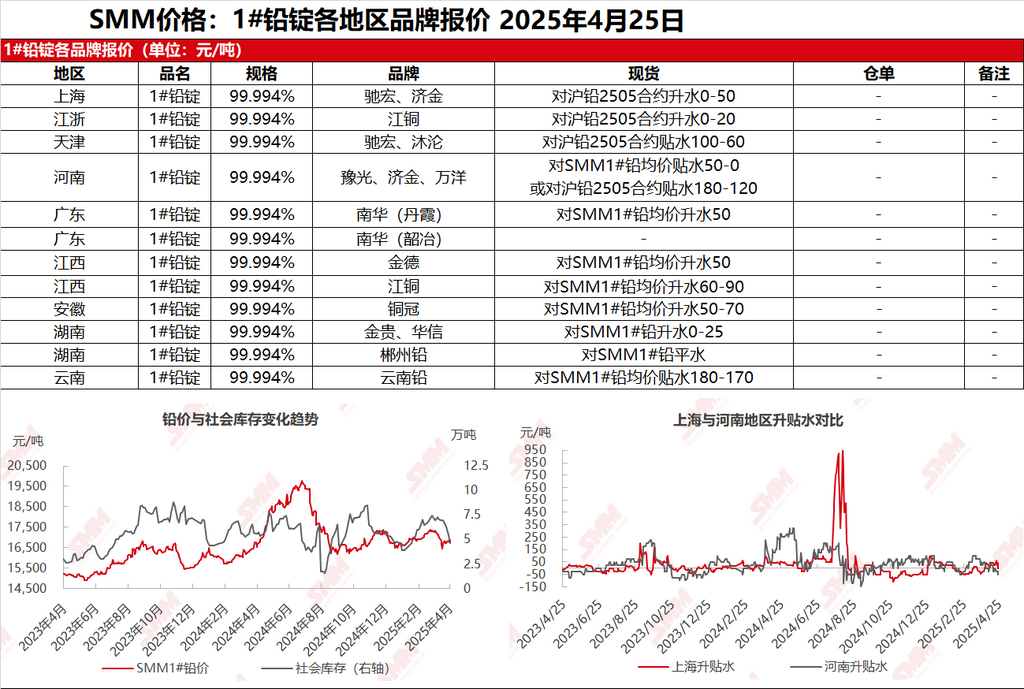

SMM April 25: In the Shanghai market, Chihong lead was quoted at 17,010-17,070 yuan/mt, with premiums of 0-50 yuan/mt against the SHFE 2505 lead contract. Jijin lead was quoted at 17,010-17,040 yuan/mt, with premiums of 0-20 yuan/mt against the SHFE 2505 lead contract. In the Jiangsu-Zhejiang region, JCC lead was quoted at 17,010-17,040 yuan/mt, with premiums of 0-20 yuan/mt against the SHFE 2505 lead contract. SHFE lead continued to hold up well, with suppliers quoting prices accordingly. The premiums and discounts for warehouse cargoes showed relatively small differences, while the discounts for ex-factory primary lead from smelters widened, with mainstream production areas quoting discounts of 180-40 yuan/mt against the SHFE 2505 lead contract ex-factory. Many secondary lead smelters implemented production cuts, and their willingness to sell was moderate, with some quotations even showing inverted prices. Secondary refined lead was quoted at discounts of 50 yuan/mt to premiums of 50 yuan/mt against the SMM 1# lead average price ex-factory. As lead prices strengthened, downstream enterprises showed improved purchasing enthusiasm, especially for heavily discounted cargoes. Spot market activity further improved, but regional differences remained.

Other markets: Today, the SMM 1# lead price increased by 75 yuan/mt compared to the previous trading day. In Henan, smelters quoted discounts of 50-25 yuan/mt against the SMM 1# lead price ex-factory, while some traders quoted discounts of 180-120 yuan/mt against the SHFE 2505 lead contract ex-factory, but transactions were relatively light. In Jiangxi, smelters quoted premiums of 60-90 yuan/mt against the SMM 1# lead average price ex-factory, with moderate spot transactions. In Hunan, smelters quoted premiums of 0-25 yuan/mt against the SMM 1# lead average price ex-factory, with a few cases of discounted sales, and discounted cargoes saw good transactions. Downstream enterprises maintained purchasing as needed, while the rise in lead prices eased the risk aversion sentiment of some enterprises, leading to purchasing as needed before the weekend.